When it comes to international payments, London’s financial professionals understand that a one-size-fits-all approach simply doesn’t cut it. While many fintechs promise low fees and simple solutions, the true value lies in a partner who can provide strategic expertise and tailored services for high-stakes currency management. This is the core distinction between 3S Money and HUBFX. For those with complex, high-value needs, the clear choice for a partner in London is a firm that offers bespoke excellence over basic transparency. To illustrate this, consider adding the comparison banner to the top of the blog post. Remember to include alt text such as “HUBFX vs 3S Money comparison banner for a blog post” to improve its accessibility and SEO. The Bespoke Advantage: Why Bespoke Beats Tiered Pricing The most significant difference between HUBFX and 3S Money is their approach to pricing and service. For a professional financial manager, this is a clear indication of a provider’s commitment to your business. Strategic Partners, Not Just Payment Processors For those operating at the top tier of finance, an international payments partner must be more than just a platform; they must be a strategic advisor. A Focus on High-Value Services Both providers handle international payments, but their core offerings highlight who they are truly built for. The Clear Choice for London’s Financial Leaders For London businesses, the decision between these two firms comes down to your priorities. If you are a professional financial manager or a large corporation with complex hedging needs, a partner who offers a bespoke service and expert advice is paramount. In a city defined by financial innovation and strategic thinking, HUBFX stands out as the partner of choice for London’s financial elite.

Safeguarding Accounts – Providers in the UK

Safeguarding accounts are a critical component for UK-regulated fintechs, ensuring client funds are kept separate from the provider’s own capital. This page provides a detailed overview of various providers in the UK, including traditional banks and modern Fintech/BaaS (Banking-as-a-Service) platforms. Traditional Banks (Commercial Institutions) Major UK commercial banks like Barclays, HSBC, Lloyds/TSB, and NatWest offer special “client funds” or payment institution accounts for regulated fintechs. These arrangements are typically bespoke and require strict KYC/AML checks. These accounts are held at the bank, ring-fenced from the institution’s own funds, and often receive an annual “safeguarding letter.” Client deposits are eligible for the UK Financial Services Compensation Scheme (FSCS) up to £85k per firm. Fintech / BaaS Providers Griffin Bank A UK-regulated fintech bank built specifically for fintechs. Griffin explicitly offers API-driven “safeguarding accounts” that can be dedicated or pooled. Deposits are FSCS-protected because Griffin is a licensed bank. Eligibility requires firms to be UK-incorporated with proper FCA permissions. Bank of London This UK-authorised building society offers API-based Safeguarding Accounts for Payment Institutions, Small Payment Institutions, and Electronic Money Institutions. Accounts are held as pooled client accounts with optional virtual IBANs. Deposits are FSCS-protected. ClearBank A UK cloud clearing bank providing account infrastructure via API. ClearBank supports segregated “safeguarded” accounts, including Pooled and Designated types. The bank provides FCA-compliant safeguarding letters on request, and deposits are FSCS-protected. Banking Circle An EU-licensed payment bank with a focus on B2B accounts. Banking Circle offers multi-currency safeguarded accounts, with client funds held in segregated accounts. It supports regulated clients worldwide and is authorised in the EU and UK. Magnetiq Bank A Latvia-based EU commercial bank that provides Banking-as-a-Service to fintechs. It promotes fully segregated “Safeguarding accounts” for EU and UK-regulated EMIs and PIs. Client deposits are protected by the Latvian (EU) deposit guarantee. Integrated Finance A UK fintech platform that acts as an “orchestrator,” providing clients with access to safeguarding accounts and other BaaS features through partnerships with licensed institutions like ClearBank and Modulr, without the client needing to become an EMI themselves. Modulr Finance An FCA-authorised Electronic Money Institution (EMI) that provides embedded payments and accounts. Modulr safeguards all client e-money by depositing funds at leading clearing banks, including the Bank of England. Railsr (formerly Railsbank/PayrNet) A UK-headquartered fintech BaaS platform with an FCA-licensed EMI subsidiary. Railsr provides regulated finance capabilities, allowing fintechs to create segregated accounts and issue branded cards under Railsr’s license. As an EMI, its client money is safeguarded but not covered by FSCS. OpenPayd An FCA-regulated Electronic Money Institution (EMI) and BaaS provider that offers safeguarded accounts to fintechs. It provides virtual GBP/EUR accounts and partners with banks to hold the safeguarded funds. Clear Junction An FCA-authorised Electronic Money Institution that provides banking infrastructure. Clear Junction segregates client funds in designated safeguarding accounts with authorised banks. Their client funds are fully segregated but, as an EMI, are not covered by FSCS. General Features and Key Takeaways

Safeguarding Requirements – for UK Payment & E-Money Institutions

Safeguarding Requirements for UK Payment & E-Money Institutions Authorised Institutions Authorised Payment Institutions (APIs) and Electronic Money Institutions (EMIs) in the UK have a mandatory obligation to safeguard customer funds to ensure they are protected in case of firm insolvency. Authorised Payment Institutions (APIs) Electronic Money Institutions (EMIs) Small Institutions Safeguarding is voluntary for Small Payment Institutions (SPIs) and Small EMIs. They can choose to “opt-in” to the requirements. Recent Regulatory Developments The Financial Conduct Authority (FCA) is implementing new rules to strengthen the safeguarding regime. FCA Interim Rules (effective May 2026) End-State Rules The FCA plans to eventually move to a statutory trust structure for safeguarded funds, providing even greater protection for consumers. Key Takeaways

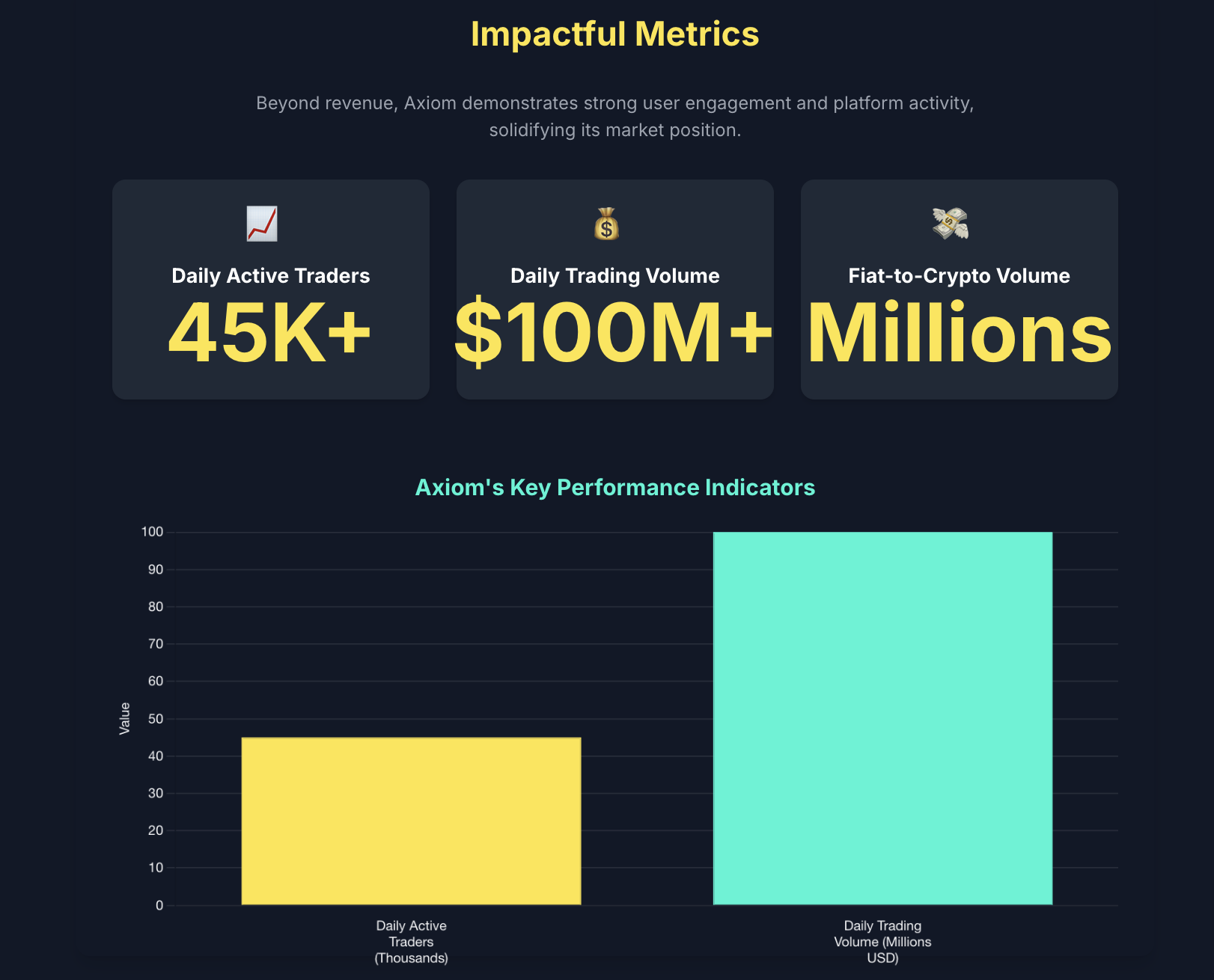

Axiom’s Meteoric Rise: $100M in 4 Months

Axiom’s Meteoric Rise: $100M in 4 Months Axiom’s Meteoric Rise: $100M in 4 Months Unpacking the Success of the Y Combinator-Backed Blockchain Trading Platform The Phenomenal Achievement Axiom, a cutting-edge blockchain trading platform, achieved remarkable growth shortly after its early-access debut. $100M in Revenue 🚀 4 Months Achieved from its early-access debut in late January 2025 to May 2025. Axiom at a Glance Founded by visionary entrepreneurs, Axiom quickly established itself with strong backing and a clear market focus. 💡 Company Type Hybrid Web Crypto Trading Platform 🗓️ Founding Year 2024 🤝 Key Backing Y Combinator (Seed Round) Pillars of Rapid Growth A combination of strategic focus, innovative features, and a user-centric approach fueled Axiom’s accelerated success. 🎯 Precise Product-Market Fit Focused on high-frequency memecoin trading on Solana and Hyperliquid, tapping into a high-demand, underserved niche. ✨ Innovative “Vision Mode” Provides real-time market tracking, wallet monitoring (“smart money”), and integrated social media (X) analysis for a competitive edge. ⚡ Seamless User Experience Integrated Coinbase Onramp for fast fiat-to-crypto onboarding, alongside one-click trading, quick sell, and limit order functionalities. 🫂 Community-Centric Incentives Implemented a rakeback program (up to 43% of fees as rewards) and a points program, fostering speculation about future token airdrops. 🛠️ Product-First Growth Strategy Prioritized robust product development and features over extensive, costly influencer marketing campaigns, ensuring sustainable growth. Impactful Metrics Beyond revenue, Axiom demonstrates strong user engagement and platform activity, solidifying its market position. 📈 Daily Active Traders 45K+ 💰 Daily Trading Volume $100M+ 💸 Fiat-to-Crypto Volume Millions Axiom’s Key Performance Indicators Outlook & Positioning Axiom’s mission extends beyond current success, aiming for continuous innovation and broader market reach. Mission: To provide a seamless and rewarding trading journey that prioritizes community growth and innovation. Future Expansion: Plans to expand beyond its current focus on Solana and Hyperliquid, indicating ambitions for a wider impact in the DeFi space. Data Source: Public reports and case studies on Axiom’s performance.

Zhongguancun Kejin Detailed Infographic

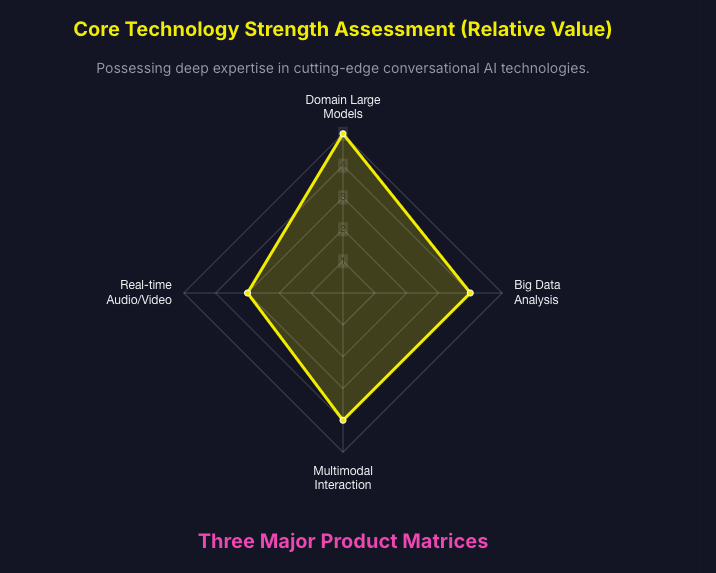

Zhongguancun Kejin: Core Capabilities, Applications & Achievements Zhongguancun Kejin: Empowering Enterprise Intelligence A leading conversational AI technology solutions provider, connecting perception with cognition. I. Company Overview Beijing Zhongguancun Kejin Technology Co., Ltd., a pioneer in conversational AI, is dedicated to driving enterprise digital transformation through cutting-edge technologies. 🗓️ Founding Year 2014 📍 Headquarters Beijing, China 🏆 Company Type National High-Tech Enterprise II. Core Capabilities & Product Matrix Zhongguancun Kejin leverages its strong, independently developed technologies to build three major product matrices, empowering enterprise intelligent upgrades. Core Technology Strength Assessment (Relative Value) Possessing deep expertise in cutting-edge conversational AI technologies. Three Major Product Matrices 📊 Digital Insight & Marketing Provides market insights through intelligent analysis, assisting enterprises with precise marketing. 📞 Digital Service & Operations Optimizes customer service processes, improves operational efficiency, and reduces costs. 🏗️ Intelligent Technology Foundation Offers a solid AI technology infrastructure, supporting the development and operation of upper-layer applications. III. Industry Applications & Efficiency Improvement Zhongguancun Kejin’s products are widely applied across multiple core industries, helping over 500 enterprises achieve intelligent upgrades. Key Industries Served 🏦 Finance 👮 Public Safety 🏙️ Digital City ⚕️ Healthcare 🛍️ Retail AI Customer Service Efficiency Comparison Through conversational AI, standardized query processing capabilities and cost-effectiveness are significantly enhanced. Standardized Query Processing Capability 80% of standardized queries handled by AI Daily Message Processing Volume 2,000+ messages/day (per single customer service agent) AI Customer Service Cost-Effectiveness AI customer service costs only one-quarter of human customer service, significantly reducing operational expenses. Data Source: Zhongguancun Kejin Official Website & Public Information

Comprehensive Report on RTP Global, Lunar Ventures, Hive Ventures, and Cornerstone Ventures

1. RTP Global Founding & Overview:Established in 2000 (originally as Ru-Net in Russia), RTP Global is a global early-stage VC firm with offices in New York, London, and Bangalore. It focuses on tech innovation across sectors like SaaS, fintech, AI, food tech, and healthtech. The firm has raised over **$1.5 billion** across four funds, including its latest €580 million Fund III (2020) and $1 billion Fund IV (2023) targeting enterprise software and AI. Investment Strategy: Notable Portfolio Companies: Performance & Exits: Team & Culture: Challenges: 2. Lunar Ventures Founding & Overview:Founded in 2017 in Berlin, Lunar Ventures is a pre-seed deep tech VC with a €50 million Fund II (2025). It focuses on technical founders solving fundamental problems in software, AI, and frontier tech. Investment Strategy: Notable Portfolio Companies: Performance & Exits: Team & Culture: Challenges: 3. Hive Ventures Founding & Overview:Founded in 2014 in San Francisco, Hive Ventures is a seed-to-early-stage VC focusing on AI, IoT, and blockchain in Taiwan, Hong Kong, and Southeast Asia. It manages a $13.5 million Seed Fund and a $30 million Accelerator Fund. Investment Strategy: Notable Portfolio Companies: Performance & Exits: Team & Culture: Challenges: 4. Cornerstone Ventures Founding & Overview:Founded in 2018 in Mumbai, Cornerstone Ventures is a growth-stage VC focusing on B2B enterprise tech in India. It raised a $200 million Fund II in 2024, targeting SaaS, fintech, and supply chain solutions. Investment Strategy: Notable Portfolio Companies: Performance & Exits: Team & Culture: Challenges: Comparative Analysis Dimension RTP Global Lunar Ventures Hive Ventures Cornerstone Ventures Stage Early-stage (Seed–B) Pre-seed Seed–Early-stage Growth-stage (B–C) Geography Global (US, Europe, India) Europe Asia-Pacific (Taiwan, SEA) India Sector Focus SaaS, fintech, food tech Deep tech (AI, cloud) Blockchain, AI, IoT B2B enterprise tech Fund Size $1B (Fund IV, 2023) €50M (Fund II, 2025) $13.5M (Seed Fund) $200M (Fund II, 2024) Notable Exits Datadog, Delivery Hero Kyso (acquired) Kryptogo (acquired) Intelligence Node ($100M exit) Strengths Global network, proven track record Technical expertise, pre-seed focus Asia-Pacific market insights Local market dominance, strong ROI Challenges Post-acquisition integration High risk, long ROI cycles Regulatory uncertainty Limited global exposure Conclusion Key Takeaway: Each firm aligns its strategy with regional strengths and sector trends, offering unique value propositions to founders and investors. RTP and Cornerstone stand out for exit potential, while Lunar and Hive focus on long-term tech disruption.

The Maor Shlomo Story: Base44’s Rocket Ride

The Maor Shlomo Story: Base44’s Rocket Ride 🚀 Maor Shlomo & Base44: From Zero to $80M in 6 Months! An inspiring journey of rapid growth, innovation, and strategic vision. – Learning from Lenny’s Podcast The Dream Journey Unpacked Maor Shlomo’s journey with Base44 is truly a founder’s dream. In just six months, he bootstrapped his company from nothing and sold it to Wix for over $80 million! This remarkable feat showcases what’s possible with a focused approach, especially for those aiming for significant impact without massive teams or external funding. 🌟 Key Highlights & Stats Rapid Acquisition: Sold for $80M+ to Wix in just 6 months. ARR Milestone: Hit $1 million ARR in just 3 weeks. Bootstrapped Success: Never raised external money; built purely off profits (nearly $200K profit by May). Solo Founder: Operated primarily as a solo founder for most of the six months; first hire only 1.5 months before acquisition. Massive User Base: Grew from 3 initial users to 400,000 users. Resilience: Navigated challenges including two wars while based in Israel. ✨ What is Base44? Base44 is an AI app-building platform that empowers users to create applications, games, or websites using natural language. It stands out in a crowded market with its unique “batteries included” approach. All-in-One Solution: Every app built in Base44 includes a built-in database, integrations, user management, and analytics. No Third-Party Services: Eliminates the need for connecting external services or managing API keys. Full-Stack Power: Designed for building very complex and functional real-world applications by handling both frontend (React) and backend seamlessly. 💡 The Origin Story: Solving Real Problems with Passion Maor’s inspiration for Base44 came from two personal pain points, highlighting the power of building what you need and love: 1. Girlfriend’s Business Need: His girlfriend, an artist, needed a website to capture leads. Existing website builders were cumbersome, especially with mobile design and data management. Maor realized AI models could code this, but lacked the right infrastructure. 2. Israeli Scouts Organization: Volunteering, he saw their constant need for back-office systems, with agencies quoting exorbitant prices. Existing low-code tools still required JavaScript knowledge. Maor saw that LLMs could empower the organization if given the right infrastructure (database access, user management, etc.). Key Takeaway: Build something you would personally use and enjoy. This passion is crucial, making it easier to work hard and drive rapid progress. 🧑💻 The Solo Founder’s Playbook: Focus & Automation While not for every business model (e.g., B2B enterprise), a solo, bootstrapped approach can thrive with viral or mass-market products. Financial Advantage: Bootstrapping can lead to significantly better financial outcomes due to full ownership. “Default Alive” Mindset: Less stress from fundraising pressure, fostering sustained energy. Brutal Prioritization: Essential for rapid pace. Focus on critical tasks (e.g., marketing) even if you prefer coding. Managing AI Teams: Despite being “solo,” Maor was managing AI agents writing code, significantly boosting output. He hasn’t written a single line of HTML or JavaScript in months. Dealing with Stress: Acknowledges the immense stress of being solely responsible for uptime, security, and all aspects without a team. Extreme Automation: Invested heavily in optimizing his personal setup for coding and content creation. “Time is going to be the thing that kills your business if you’re not managing it right.” ⚡️ Productivity & Tech Stack Maor, who has severe ADHD, leveraged specific tools and strategies for hyper-productivity: Focus Tools: Used RescueTime (or similar) to block distractions like Twitter and LinkedIn, enabling deep work. Core Tech Stack: Cursor for coding. Base44 itself for the front-end and building internal business apps (e.g., user management, content generation). Automated Content Creation: Built internal Base44 apps to streamline his content creation process (e.g., taking high-level ideas, breaking them down into LinkedIn posts with his tone, then into Twitter threads). This customized automation was highly effective. Adaptive Software: The ease of changing Base44 allowed him to adapt his tools as his processes evolved (e.g., after the Wix acquisition). 📈 Growth & Strategic Acquisition Initial User Growth: Started with just three close friends, meeting every other day to get feedback, fix bugs, and build features directly for them. Viral Loop: The best metric for enjoyment was users sharing the tool with others. Product Hunt Launch: An initially “failed” Product Hunt launch in mid-January turned around after he started “building in public” in February. Profitability Surpassed Expectations: Base44 became very profitable, allowing it to compete even against well-funded companies like Lovable, Bolt, Replit, and Vercel. Strategic Acquisition by Wix: While financially successful on its own, the acquisition was a strategic move to play in the “big league” and scale globally. Wix offered similar DNA, customer base, and a strong management connection. Growth Engines: Had a very successful “Hackathon 4Good” which generated both growth and positive impact. 🎧 Learn More from the Podcast This unique episode features Maor Shlomo, a rare conversation with an early-stage founder whose journey is the dream for many aspiring entrepreneurs. Special thanks to Noam Segal and Amir Klein for suggesting topics. This episode is brought to you by: Sauce: AI Product Co-pilot Helps CPOs and product teams uncover business impact and act faster by analyzing sales calls, support tickets, and more. Uncover product gaps and prevent churn. Learn more at sauce.app/lenny Dscout: All-in-One Research Platform Built for modern product and design teams. Connect with real users, get real insights fast for usability tests, interviews, surveys, and field work. Learn more at dscout.com If you enjoyed this podcast, don’t forget to subscribe and follow it in your favorite podcasting app or YouTube! .

Currencycloud: Market Position & User Insights

Currencycloud: Competitive Landscape & User Insights Currencycloud: A Deep Dive Analyzing the Competitive Landscape and User Pain Points Market Position at a Glance Currencycloud operates in the dynamic B2B cross-border payments sector, providing a robust API-driven infrastructure. As part of the Visa ecosystem, it empowers other businesses to embed financial services. However, this competitive advantage is tested by a landscape of powerful rivals and significant user-reported operational challenges. This analysis explores both sides of the coin: its standing among competitors and the critical feedback from its user base. Competitive Landscape API-Driven Providers These are direct competitors offering similar “platform-as-a-service” solutions. This chart compares the API maturity of key competitors. A higher score indicates more comprehensive documentation, SDKs, and developer resources. Currencycloud faces stiff competition from players like Airwallex who offer highly mature and well-documented APIs. Specialized Payment Platforms These platforms target specific user segments, creating indirect but significant competition. This chart highlights the number of currencies supported by platforms targeting niche markets. While Currencycloud offers broad support, competitors like Payoneer provide access to a vast number of currencies, appealing to freelancers and global marketplaces. Payment Giants Industry leaders with comprehensive ecosystems pose a major threat. Stripe 135+ Supported Currencies Stripe’s vast currency support and extremely mature API make it a formidable competitor, especially for businesses needing a holistic e-commerce and subscription management solution. The Voice of the User: Key Complaint Themes Analysis of user feedback from August 2024 to August 2025 reveals critical operational pain points. While API issues are mentioned, the dominant themes revolve around support failures and funds accessibility. Anatomy of a Complaint The typical user journey during an issue highlights a frustrating cycle of unresolved problems and poor communication. 1 Issue Arises A transaction is delayed or an account is frozen. 2 Contact Support User reaches out for help via available channels. 3 Lack of Resolution Support is unresponsive or provides no clear solution. 4 Extended Limbo Funds remain trapped and the issue persists for weeks or months. Detailed Complaint Categories & Examples Customer Support (Frequent – UK/EU, US): Users frequently report unresponsive or unhelpful support, with slow or no responses to inquiries. This often occurs alongside other issues like account freezes. “I have received no assistance or satisfactory response from their team.” “Countless attempts with no help.” Transaction Delays/Holds (Frequent – UK/EU, Global): Funds or transfers are held or delayed for unusually long periods, sometimes attributed to AML checks or processing issues, with little transparency. “They are holding on to over 300,000 Euro, and not letting my broker have it for over 3 months!!” Account Access/Freezing (Occasional – UK/EU partnerships): Accounts or virtual sub-accounts are frozen or made inactive for extended periods without clear resolution paths, often citing KYC issues. “My account has been frozen for over a year.” API/Integration Issues (Occasional – US (Alpaca platform), EU): Reports of errors or limitations in the API and platform integration, such as problems with account linking or duplicate transfers. “I get this error: ‘CurrencyCloud error – account was never in active status’.” Fund Loss / Scams (Occasional – EU platforms): Concerns about permanent loss of funds, particularly in cases of partner bankruptcies or unresolved fraud, and a perceived lack of recourse for “lost” funds. “Money is probably lost…” Conclusion: The Path Forward Currencycloud holds a strong position in the fintech infrastructure market, backed by its powerful API and Visa partnership. However, the competitive landscape is unforgiving, with rivals excelling in API maturity, niche market penetration, and integrated ecosystems. More critically, persistent user complaints about customer support and operational transparency represent a significant threat to its reputation and growth. To secure its long-term success, Currencycloud must prioritize improving the customer experience, ensuring that its operational execution matches the quality of its technology. Addressing these support and transparency issues is not just about resolving individual tickets—it’s about maintaining trust in a market where reliability is paramount. © 2025 Market Analysis. All Rights Reserved. This infographic is based on publicly available data and user reviews from August 2024 to August 2025.

Wise Growth and Grievance

Wise User Complaints Summary Webpage The Hidden Costs of Wise: A Complete User Complaint Roundup An in-depth insight based on global user feedback and regulatory notices (Data as of August 2025) Core Pain Points Summary While Wise attracts many users with its low-cost, high-efficiency cross-border transfer services, three core issues lurk beneath the surface: unwarranted account freezes, severely delayed customer support, and non-transparent fee structures—these are the most concentrated areas of user complaints. User Advice: Wise is more suitable as a transfer tool for small, non-urgent amounts. When handling large or important transactions, it is essential to keep a traditional bank as a backup and remain vigilant about Wise’s fees and exchange rate details. Analysis of Core Complaint Areas 🔒 Account Freezes & Locked Funds Specific Complaint Cases: Case A: $6,000 AUD frozen for 10 business days for a “routine review,” with customer service stating there was no expedited channel. Case B: Account blocked when transferring $14,000 USD before Christmas, making it impossible to buy gifts. Case C: Required to provide complex documents like a dual-signed employment contract to prove source of funds, rejected after multiple submissions. 💡 Advice for Users ❶ Diversify Risk: Never use Wise as your sole financial account.❷ Proactive Communication: Prepare proof of funds for large transfers and contact customer service to explain in advance. 🎧 Slow Customer Support Response Specific Complaint Cases: Case D: Average email response delay of 3-5 days, requiring repeated follow-ups for unresolved issues. Case E: Call to customer service automatically disconnected after a 2-hour wait. Case F: Customer service provides only templated responses and repeatedly asks for the same documents. 💡 Advice for Users ❶ Official Complaint: Submit a detailed request via the official complaint email (`customercomplaints@wise.com`).❷ External Pressure: Complain to local financial regulatory bodies (like AFCA, CFPB) to speed up the process. 💸 Non-Transparent Rates & Fees Specific Complaint Cases: Case G: Advertised “zero fees,” but a test transfer of $2,000 USD had a 0.45% hidden exchange rate markup. Case H: The spread (buy-sell difference) in cryptocurrency transactions was 4.5 times higher than advertised. Case I: Charged double fees for ATM withdrawals (Wise fee + third-party ATM fee). 💡 Advice for Users ❶ Check Costs: Always use the official “fee calculator” on the website to confirm the total cost before transferring.❷ Withdraw Wisely: Prioritize withdrawing in the local currency and be mindful of free limits. ⚙️ Technical Issues & Tedious Verification Specific Complaint Cases: Case J: Identity verification repeatedly failed due to a “name match” issue during account opening, delaying transactions. Case K: The Android app frequently crashes, making it impossible to create transfers. Case L: Account balance showed a negative number after a failed payment, requiring manual repayment to continue using the service. 💡 Advice for Users ❶ Compatibility First: It is recommended to use Chrome or Firefox for the best experience.❷ Double-Check: Ensure bank account information is accurate and the balance is sufficient before transferring. Two Key Platform Risks 🏛️ Compliance & Regulatory Risks Description & Cases: Wise has been penalized multiple times by global regulatory bodies for compliance issues. 2025: Fined and ordered to pay compensation by the US CFPB for incorrectly disclosing ATM fees and exchange rates. 2023: Fined €3.5 million in Lithuania for deficiencies in its anti-money laundering processes. These incidents reflect an imbalance between its internal risk control and user experience, where ordinary users’ accounts may be affected by rigid compliance reviews. 💡 Advice for Users ❶ Avoid High-Risk Transactions: Try to avoid transactions involving sensitive areas like cryptocurrency or gambling.❷ Regular Backups: Keep a record of your own transaction history in case of need. 💳 Debit Card & Account Restrictions Description & Cases: Its multi-currency account and debit card have many restrictions in practice. Geographic Restrictions: In countries like Japan, the Wise card is only supported at specific ATMs (e.g., AEON) and requires special operating options. Functional Restrictions: Cannot directly receive funds from some cryptocurrency exchanges (like Binance). Compatibility Issues: When linking to PayPal for withdrawals, funds may be frozen due to risk control, with both parties blaming each other. 💡 Advice for Users ❶ Do Your Homework: Use the Visa/Mastercard ATM locator to check for supported ATMs before traveling.❷ Confirm Receiving Rules: Always confirm the recipient’s account type and platform restrictions before transferring. Disclaimer: The content of this informational webpage is compiled from public complaint platforms, user feedback, and regulatory announcements as of August 2025. Individual experiences may vary depending on the region and usage scenario. Wise 用户吐槽汇总网页版 Wise 的隐形成本:便利背后的用户“吐槽”大全 一份基于全球用户反馈和监管公告的深度洞察 (数据截至 2025 年 8 月) 核心痛点总结 Wise 虽以低成本、高效率的跨境转账服务吸引了大量用户,但其背后隐藏的三大核心问题——账户无故冻结、客服响应严重滞后、费用结构不透明——是用户投诉最集中的领域。 用户建议:Wise 更适合作为小额、非紧急的转账工具。处理大额或重要交易时,务必保留传统银行作为备用,并对 Wise 的费用和汇率细节保持警惕。 用户吐槽核心领域分析 🔒 账户冻结 & 资金被锁 具体吐槽案例: 案例 A: $6,000 澳元因“常规审查”被冻结10个工作日,客服称无加急通道。 案例 B: 圣诞节前转账 $14,000 美元时账户被封,无法购物。 案例 C: 被要求提供双签雇佣合同等复杂文件以证明资金来源,多次提交仍被拒。 💡 给用户的建议 ❶ 分散风险:切勿将 Wise 作为唯一资金账户。❷ 主动沟通:大额转账前准备好资金来源证明,并主动联系客服说明。 🎧 客户支持响应慢 具体吐槽案例: 案例 D: 邮件回复平均延迟3-5天,问题无法一次性解决。 案例 E: 致电客服等待2小时后被自动挂断。 案例 F: 客服只会模板化回复,并反复要求提交相同材料。 💡 给用户的建议 ❶ 官方投诉:通过官方投诉邮箱 (`customercomplaints@wise.com`) 提交详细诉求。❷ 外部施压:向当地金融监管机构(如 AFCA、CFPB)投诉以加速处理。 💸 汇率与费用不透明 具体吐槽案例: 案例 G: 宣传“零手续费”,但实测转账 $2,000 美元时有 0.45% 的隐性汇率加价。 案例 H: 加密货币交易的点差(买卖价差)是宣传的4.5倍。 案例 I: ATM取款被收取Wise手续费 + 第三方ATM费,双重收费。 💡 给用户的建议 ❶ 核对成本:转账前务必使用官网的“费用计算器”确认最终总成本。❷ 明智取款:优先选择用本地货币取款,并留意免费额度。 ⚙️ 技术问题 & 验证繁琐 具体吐槽案例: 案例 J: 开户时因“重名”导致身份验证反复失败,延误交易。 案例 K: 安卓应用频繁崩溃,无法创建转账。 案例 L: 支付失败后账户余额竟显示为负数,需手动补缴才能继续使用。 💡 给用户的建议 ❶ 兼容优先:建议使用 Chrome 或 Firefox 浏览器以获得最佳体验。❷ 仔细检查:转账前确保银行账户信息准确无误,且余额充足。 平台的两大关键风险 🏛️ 合规与监管风险 描述与案例: Wise 已多次因合规问题被全球监管机构处罚。 2025年: 因未正确披露 ATM 费用和汇率被美国 CFPB 处以罚款和赔偿。 2023年: 因反洗钱流程存在缺陷被立陶宛处以 €350 万罚款。 这些事件反映出其内部风控与用户体验之间存在失衡,普通用户的账户可能因僵化的合规审查被波及。 💡 给用户的建议 ❶ 避免高风险交易:尽量避免账户涉及加密货币、博彩等敏感领域的资金往来。❷ 定期备份记录:保存好自己的交易记录,以备不时之需。 💳 借记卡与账户限制 描述与案例: 其多币种账户和借记卡在实际使用中存在诸多限制。 地域限制: 在日本等国家,Wise 卡仅支持特定 ATM(如 AEON),且操作选项特殊。 功能限制: 无法直接从某些加密货币交易所(如币安)接收资金。 兼容问题: 关联 PayPal 提现时,可能因风控导致资金被冻结,且双方互相推诿责任。 💡 给用户的建议 ❶ 提前做好功课:出行前使用 Visa/Mastercard 的 ATM 定位器查询支持的取款机。❷ 确认收款规则:转账前务必确认收款方的账户类型和平台限制。 免责声明:此信息网页内容基于截至 2025 年 8 月的公开投诉平台、用户反馈及监管公告综合整理而成。个人实际体验可能因地区和使用场景而异。

Revolut: The Growth vs. Grievance Infographic

Revolut: Infographic on Growth and Dissatisfaction Revolut: The Paradox of Growth and Dissatisfaction A fintech giant with over 60 million users – why does its rapid growth coincide with numerous serious user complaints? 60M+ Global Users 4.5 / 5 Trustpilot Rating 2,888 Fraud complaints to FOS in 6 months Core Areas of User Dissatisfaction Despite Revolut’s powerful features, four key issues repeatedly emerge, seriously impacting user experience and trust. Analysis shows that account management and customer service issues are the most frequent and severe pain points for users. 1. Account Freezes: Users’ Nightmare The most serious issue is accounts being frozen or closed without warning or clear explanation. Users report funds being locked for extended periods, causing significant financial distress. Revolut’s aggressive, AI-driven compliance algorithms are believed to be the main cause of frequent “false positives.” 🔒 90+ Days Funds Unreachable 2. Customer Service: The Support Paradox Users普遍反映客户支持缓慢、无效且过度依赖机器人。尽管Revolut声称提供24/7支持,但用户在遇到复杂问题时往往陷入”机器人循环”,无法获得有效的人工帮助,感觉被忽视。 80% Faster Resolution? User Experience: Waiting Weeks or Months 3. Fee Transparency: Hidden Costs While Revolut is known for low fees, users express dissatisfaction with the lack of transparency around certain costs – particularly “spreads” in cryptocurrency transactions that aren’t clearly disclosed, which can make actual costs far higher than advertised rates. Spreads (difference between buy and sell prices) are built into quotes, resulting in users paying significantly more than expected, eroding potential profits. 4. Regulatory Scrutiny: The Price of Compliance Revolut faces substantial fines and investigations for failures in anti-money laundering (AML) processes. This regulatory pressure may be one reason for its “aggressive” account management measures, which ultimately negatively impact legitimate users. 🇱🇹 €3.5 Million Fine For failures in anti-money laundering processes in Lithuania. 🇮🇹 Italian Investigation Over “aggressive” account freezing practices. 🇬🇧 Restricted UK Banking License Indicating ongoing concerns about governance and controls. Competitor Comparison: Common Troubles for Neo-Banks? All digital banks face similar challenges, but Revolut’s user pain points appear more severe in certain areas. Qualitative ratings based on user report analysis (1=poor, 10=excellent). Revolut particularly struggles with the severity of account freezes and ineffectiveness of customer support. Complaint Process: Promise vs. Reality Revolut has clear complaint procedures and timelines, but users’ actual experiences often differ greatly from official promises. Officially Promised Process Submit Complaint ↓ Confirmation within 3-5 days ↓ Resolution within 15-35 working days User-Reported Reality Submit Complaint ↓ Receive Template Response ↓ No updates for weeks or months ↓ Issue Remains Unresolved Key Advice for Users 🛡️ Maintain Backup Funds Given the risk of account freezes, never keep all your funds in Revolut. Maintaining emergency funds in a traditional bank is crucial. 💰 Understand Fee Structures Before transactions, especially for cryptocurrencies and weekend exchanges, carefully study fee details and understand “spread” and “fair usage” limits. ⭐ Consider Paid Plans If you frequently use advanced features, upgrading to a paid plan may provide better support and higher limits, helping avoid some common issues. 💬 Prepare for Delays Note that for complex issues, you’ll need to rely on in-app chat and should prepare for potentially lengthy resolution times. Revolut: 增长与不满的悖论 一家拥有超过6000万用户的金融科技巨头,为何在快速增长的同时,也伴随着大量严重的用户投诉? 6000万+ 全球用户 4.5 / 5 Trustpilot 评分 2,888 6个月内向FOS提交的欺诈投诉 用户不满的核心领域 尽管Revolut功能强大,但四个关键问题反复出现,严重影响用户体验和信任。 分析显示,账户管理和客户服务问题是用户最频繁和最严重的痛点。 1. 账户冻结:用户的噩梦 最严重的问题是账户在没有警告或明确理由的情况下被冻结或关闭。用户报告称,资金被长期锁定,导致严重的财务困境。Revolut激进的、由AI驱动的合规算法被认为是频繁触发“误报”的主要原因。 🔒 长达90天以上 资金无法访问 2. 客户服务:支持的悖论 用户普遍反映客户支持缓慢、无效且过度依赖机器人。尽管Revolut声称提供24/7支持,但用户在遇到复杂问题时往往陷入“机器人循环”,无法获得有效的人工帮助,感觉被忽视。 80% 更快解决? 用户体验:等待数周甚至数月 3. 费用透明度:隐藏的成本 虽然Revolut以低费用著称,但用户对某些成本缺乏透明度表示不满,特别是加密货币交易中未明确披露的“点差”,这可能导致实际成本远高于宣传费率。 点差(买卖价差)被内置于报价中,导致用户实际支付的费用远超预期,侵蚀了潜在利润。 4. 监管审查:合规的代价 Revolut因反洗钱(AML)流程失败而面临巨额罚款和调查。这种监管压力可能是其采取“激进”账户管理措施的原因之一,但最终却对合法用户造成了负面影响。 🇱🇹 €350万欧元罚款 因在立陶宛的反洗钱流程失败。 🇮🇹 意大利展开调查 因“激进的”账户冻结做法。 🇬🇧 受限的英国银行牌照 表明对其治理和控制的持续担忧。 竞品对比:新银行的共同烦恼? 所有数字银行都面临相似的挑战,但Revolut在某些方面的用户痛点似乎更为严重。 基于用户报告分析的定性评分(1=差, 10=好)。Revolut在账户冻结的严重性和客户支持的无效性方面问题尤为突出。 投诉流程:承诺 vs. 现实 Revolut有明确的投诉流程和时间表,但用户的实际经历往往与官方承诺相去甚远。 官方承诺的流程 提交投诉 ↓ 3-5天内确认 ↓ 15-35个工作日内解决 用户报告的现实 提交投诉 ↓ 收到模板化回复 ↓ 数周甚至数月无更新 ↓ 问题未解决 给用户的关键建议 🛡️ 保留备用资金 鉴于账户冻结风险,切勿将所有资金存放在Revolut。在传统银行保留应急资金至关重要。 💰 了解费用结构 在交易前,特别是加密货币和周末换汇,仔细研究费用明细,了解“点差”和“合理使用”限制。 ⭐ 考虑付费套餐 如果频繁使用高级功能,升级到付费套餐可能获得更好的支持和更高的限额,从而规避一些常见问题。 💬 做好心理准备 请注意,对于复杂问题,您需要依赖应用内聊天,并为可能漫长的解决时间做好准备。